Managing Cash Flow Merritt – Logan Lake and Kamloops

Jen Schell

Jen SchellManaging Cash Flow Merritt – The First Pillar of Financial Planning

“If we arrange our retirement income correctly we can lower the tax we pay over our retirement and, eventually, lower the amount of taxes due at our passing on.”

Managing Cash Flow in Merritt, BC – Last edition we looked from a high level overview at the 6 pillars of financial planning. This edition will focus a little more in depth into the financial pillar of managing cash flow.

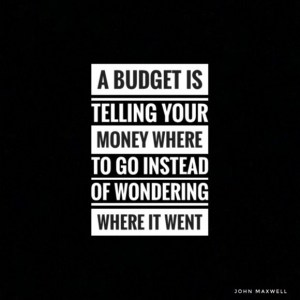

Budgets are just guides. We are in control of how they flow.

Managing Cash Flow Begins With A Cash Flow Analysis

Managing cash flow in Merritt, or anywhere else, varies over our pre-retirement and retirement years. No matter the season of life, the process remains the same.

First, we need to determine all the sources of income that we have entering our picture. Then we need to determine our current and future expenses. This can be tricky as future expenses will increase due to inflation and the loss of purchasing power takes place on our retirement nest egg.

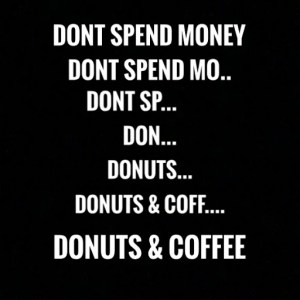

To coffee, or not to coffee…that is the question…

Managing Our Income In Our Pre-retirement Years

In our pre-retirement years, income will come in different ways. We will earn employment income, rental income or income from being self-employed. If incorporated the income may come through dividends. We could even receive capital gains from our investments. These are all taxed differently and the goal is to bring them “into our picture” in the most tax efficient manner. For the most part, if planned properly, we are in control of how we receive these and even when.

How We Determine Our Retirement Paycheque

In retirement we could still receive any of the incomes listed above. There are a few additional benefits that become available in our sixties. Firstly, between the ages of 60 and 70 we can begin receiving CPP or Canada Pension Plan benefits. If you receive the benefit before age 65, you will receive a penalty of 0.6% per month that it is taken early. Alternatively, each month after 65 that you delay receiving CPP you are paid a 0.7% bonus for life.

Secondly, between age 65 and age 70 we can begin receiving OAS or Old Age Security. Thirdly, the year we turn 71, it is mandatory that by December 31st of that year any RRSP’s, or Registered Retirement Saving Plan’s, are converted into RRIF’s, or Registered Retirement Income Funds. The government determines the mandatory minimum amount that must be withdrawn on an annual basis. Confusing? You bet it is! Fourthly, there is even a GIS, or Guaranteed Income Supplement, available in the mid to late sixties to those who can qualify for it.

Always just a phone call away.

“Why Would I Wait To Receive Government Benefits?”

A common question I am asked. It is uniquely situational. Each individual or couple has different things that are available at different times in their life. Some are struggling to make ends meet when they reach 60 years old and just take the CPP benefit early. Others may be receiving payouts upon their retirement and delaying additional income a year may be beneficial. Most answers are based on tax strategies when it comes to planning in this area. There is no cut and dry best time to take it for everyone. It must be something that is analyzed and planned for.

Some Things To Have In Place Before Retirement

Most of us will be at the height of our earning years before retirement. If planned for, we could see ourselves entering retirement mortgage free. There is no better time to have a line of credit or credit solution in place “just in case” we may need it in retirement. Credit solutions always look at what you own and what you earn. However, if you wait until you are already retired it will reduce the credit you have available.

Tax-efficiency Is Key In Retirement Income Planning

There are many strategies for income planning in retirement. Again, all are uniquely situational. Similar to questions raised above like, “When do I start collecting CPP or OAS?” These are big picture questions. It is all tied in together. Taxes are the single largest expense of our lifetime. If we arrange our retirement income correctly we can lower the tax we pay over our retirement and, eventually, lower the amount of taxes due at our passing on.

These Decisions Have Lasting Effects,

Seek Professional Help To Get It Right!

Managing Cash Flow – Nicola Valley

Financial Planning Near Merritt, BC

Managing your cash flow Merritt

Nicola Valley BC Canada

Nicola Valley Financial Planning in and around Merritt British Columbia, Canada

Merritt British Columbia Canada Top Travel Guides

Places To Stay in Merritt

Bringing solutions to Mass Affluent & High Net Worth Families

What are your goals?

Early Retirement?

Pay less taxes?

Making sure your family is taken care of?

Succession planning?

I can help!

kyle.schell@ig.ca

(250) 879-6306

- Winter Activities – Logan Lake - February 26, 2021

- Estate Planning in Merritt – Kamloops – Logan Lake - October 29, 2020

- Managing Cash Flow Merritt – Logan Lake and Kamloops - September 17, 2020

Leave a Reply

Want to join the discussion?Feel free to contribute!