Estate Planning in Merritt BC

A Holistic View on Estate & Insurance Planning in Merritt – Kamloops -Logan Lake

The Second Pillar of Financial Planning

Estate Planning in Merritt, BC – Life is full of unexpected turns and twists. Because of that, we need to have a plan in place. Here we focus on developing comprehensive strategies that protect, preserve and provide for those that we care about. What is in place to protect our income and wealth? On our passing, is there enough liquidity in our estate? Is our will up to date? Is the executor and power of attorney we selected up to the task? If we could no longer work and were not an ideal retirement age, how would our retirement look?

Great care needs to be taken to ensure the needs are all protected and fulfilled.

A Quick Disclaimer…

Some of the strategies that I will discuss are not to be taken as advice for your unique needs. I strongly suggest that you speak to a qualified professional. These are complicated issues and not to be taken lightly. Being dually licensed in Mutual Funds and Insurance, I look at the big picture when it comes to making recommendations.

Some Basic Assumptions to Begin Financial Planning

To begin, every financial plan looks at a couple main points. We start with a desired retirement date and a projected date of passing. For some, this number may be larger than others. Family history and current health are indicators of potential life expectancies. For the most part, I look at tables and project that way. A truth we must face, some of us will live to be 90 and even 100 years old.

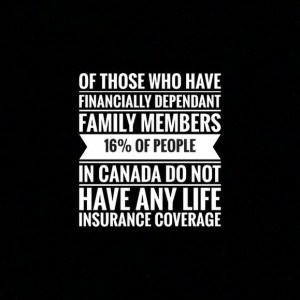

A Shocking Canadian Statistic

Protecting Our Income and Our Wealth

Play along with me for a moment. Imagine yourself 45 years old. You are in the prime earning years of your life. With possibly 20 years to go until retirement, many things are on your mind. Funding our children’s future education goals, paying off that mortgage and investing for retirement most likely top that list. You receive a call, letting you know your spouse was in a serious car accident. They unfortunately will not survive their injuries. I know this may seem grim, however, this is a part of life for some. This event was one of two things, planned or unplanned. Having a policy in place to protect against such an event will make all the difference for that surviving spouse and those children.

Estate Liquidity Needs

When an individual passes, expenses come up out of no where that need to be covered by someone. Assets like a primary residence or an investment account will not be available right away to help cover some of these expenses. If there is no will in place, your loved ones may have to cover your expenses for months to come before the courts will actually grant someone the ability to simply act as your administrator. With accounts frozen, these expenses will have to be paid out of pocket by someone else. Not exactly the lasting memory we wish to leave behind. However, a simple beneficiary designation in the correct direction or a life policy could change this whole story.

Estate Planning in Merritt and Trust Advisory (Wills/POA)

Your last will and testament is an important thing to have in place. However, just as important is who you name to carry out your last wishes. Is this executor or executrix up to the task? With your passing, could you see them being mentally and physically able to carry out this task? Not exactly something we want to take lightly. Trusts are a complicated topic as well and the situation needs to warrant having something like this in place. Split families and second marriages bring a level of complexity to the estate planning process also. The wording needs to be very accurate to ensure your wishes take place.

Living Benefits (Disability/Critical Illness/Long Term Care)

What would happen to our family if we were injured before retirement? This can have a massive impact on an individual or a family. What happens when one no longer has the ability to meet our current expenses, possibly even having expenses increase? What if a medical diagnosis or disease left us unable to earn a living for ourselves? There are so many situations that can be planned for. Ensuring we have proper coverage at different parts of our life is vitally important. Would our significant other be able to live comfortably if we needed long term care?

Ensure Your Plan Prepares You For The Unexpected

Experience Nicola Valley Financial Blogger

Estate Planning in Merritt BC

Merritt British Columbia Canada Top Travel & Adventure Guides

“Experience Community Program” (small and rural community authentic content marketing program) is a product of the EH? Tourism Marketing Group. Contact us for more information on this program at media(at)ehcanadatravel(dot)com.